All Categories

Featured

Table of Contents

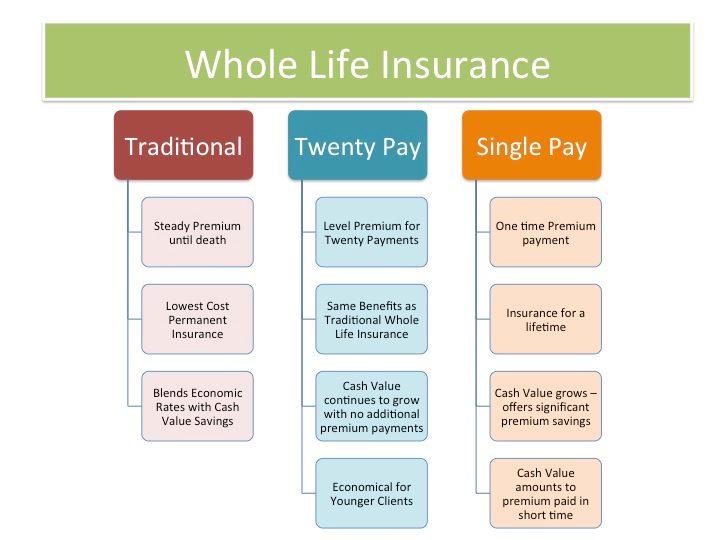

The are entire life insurance policy and universal life insurance policy. expands money worth at an assured rate of interest and also through non-guaranteed returns. grows cash money worth at a fixed or variable rate, depending upon the insurance provider and plan terms. The money value is not included to the fatality advantage. Cash worth is a feature you capitalize on while alive.

After 10 years, the cash money worth has expanded to approximately $150,000. He gets a tax-free car loan of $50,000 to begin an organization with his sibling. The plan finance rates of interest is 6%. He repays the loan over the following 5 years. Going this course, the rate of interest he pays returns into his plan's money worth instead of a banks.

Ibc Private Bank

Nash was a finance expert and fan of the Austrian college of business economics, which advocates that the worth of products aren't explicitly the result of conventional economic structures like supply and need. Instead, people value cash and items differently based on their financial standing and needs.

One of the challenges of conventional banking, according to Nash, was high-interest rates on fundings. Long as financial institutions set the rate of interest rates and loan terms, people didn't have control over their very own riches.

Infinite Banking requires you to have your economic future. For ambitious people, it can be the ideal financial device ever before. Here are the advantages of Infinite Financial: Perhaps the solitary most beneficial element of Infinite Financial is that it enhances your cash money flow.

Dividend-paying whole life insurance policy is really low threat and supplies you, the policyholder, a terrific offer of control. The control that Infinite Financial supplies can best be grouped right into 2 categories: tax benefits and asset protections.

Bank On Yourself Whole Life Insurance

When you use entire life insurance policy for Infinite Financial, you get in right into a private contract between you and your insurance provider. This personal privacy supplies specific possession defenses not found in other economic lorries. These protections might vary from state to state, they can include defense from asset searches and seizures, defense from judgements and defense from creditors.

Whole life insurance coverage policies are non-correlated properties. This is why they function so well as the monetary structure of Infinite Banking. No matter of what occurs in the market (supply, genuine estate, or otherwise), your insurance coverage policy keeps its worth.

Whole life insurance coverage is that third container. Not only is the rate of return on your entire life insurance coverage plan ensured, your death advantage and premiums are additionally assured.

This structure lines up flawlessly with the concepts of the Perpetual Wide Range Method. Infinite Financial attract those looking for higher financial control. Here are its primary benefits: Liquidity and availability: Plan finances give immediate accessibility to funds without the limitations of conventional bank loans. Tax obligation performance: The cash money worth expands tax-deferred, and policy fundings are tax-free, making it a tax-efficient device for constructing wealth.

Infinite Banking Policy

Asset security: In many states, the cash money worth of life insurance policy is safeguarded from financial institutions, including an additional layer of economic safety. While Infinite Banking has its advantages, it isn't a one-size-fits-all remedy, and it comes with considerable disadvantages. Right here's why it might not be the very best method: Infinite Financial typically requires elaborate policy structuring, which can puzzle insurance policy holders.

Visualize never ever needing to stress over small business loan or high rates of interest once again. What if you could borrow money on your terms and construct wealth at the same time? That's the power of infinite financial life insurance policy. By leveraging the money worth of entire life insurance policy IUL policies, you can grow your wide range and obtain money without relying upon conventional banks.

There's no set lending term, and you have the freedom to pick the repayment schedule, which can be as leisurely as settling the finance at the time of death. This versatility includes the maintenance of the car loans, where you can go with interest-only payments, maintaining the financing equilibrium flat and manageable.

Holding money in an IUL fixed account being credited rate of interest can typically be far better than holding the cash money on down payment at a bank.: You have actually constantly desired for opening your very own pastry shop. You can obtain from your IUL policy to cover the preliminary expenses of leasing a space, acquiring devices, and working with team.

Infinite Bank Statement

Individual fundings can be gotten from conventional financial institutions and credit rating unions. Borrowing money on a credit card is usually extremely pricey with yearly portion rates of rate of interest (APR) often getting to 20% to 30% or more a year.

The tax obligation therapy of plan fundings can differ considerably depending on your country of house and the details regards to your IUL plan. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, plan loans are generally tax-free, using a considerable benefit. In various other territories, there might be tax obligation ramifications to take into consideration, such as potential taxes on the loan.

Term life insurance coverage only provides a death advantage, without any cash money value buildup. This implies there's no cash money worth to obtain versus. This post is authored by Carlton Crabbe, Principal Exec Policeman of Resources permanently, a specialist in providing indexed global life insurance policy accounts. The info offered in this write-up is for instructional and informational purposes only and should not be construed as monetary or financial investment guidance.

For finance policemans, the extensive laws imposed by the CFPB can be seen as difficult and limiting. First, finance policemans usually say that the CFPB's policies create unnecessary red tape, resulting in more paperwork and slower financing handling. Rules like the TILA-RESPA Integrated Disclosure (TRID) policy and the Ability-to-Repay (ATR) needs, while targeted at safeguarding consumers, can lead to delays in shutting bargains and boosted operational expenses.

{kind=link}

Latest Posts

Royal Bank Visa Infinite Avion Travel Insurance

Infinite Banking Examples

Be Your Own Bank Series